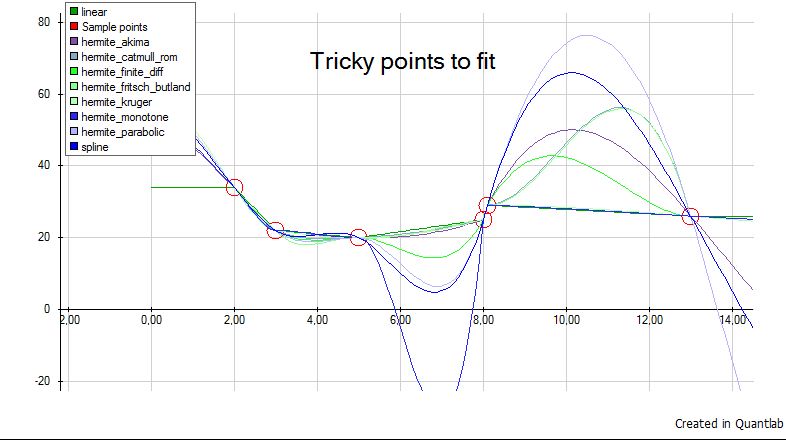

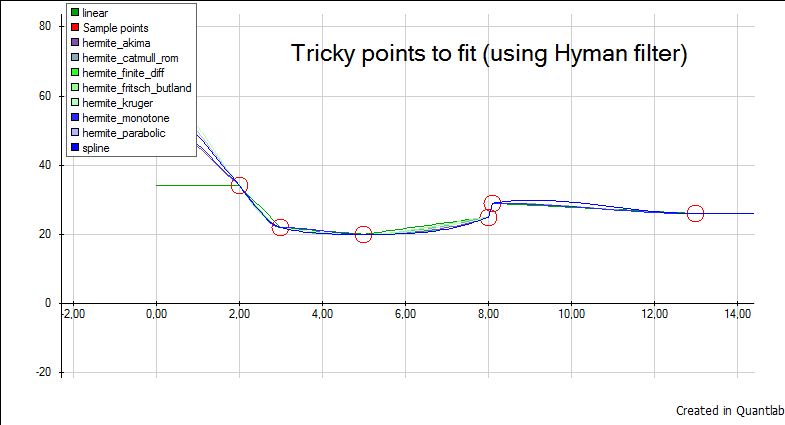

The blogger Brain Twitter has created a great example showing the benefits of using Hyman filter in yield curve interpolation. Check out: curve-fitting-with-hyman-monotonicity

I reproduce the graphs below.

This is before the Hyman filter is applied: